Realigning the Bank Branch for the New Normal with Analytics

COVID-19 has caused significant constraints on the bank branch channel with temporary closures and service limits—while moving nearly half of the branch interactions to digital channels and contact centers.

These developments present banking leaders with new risks and strategic challenges for realigning branch delivery and resources.

Survey Results

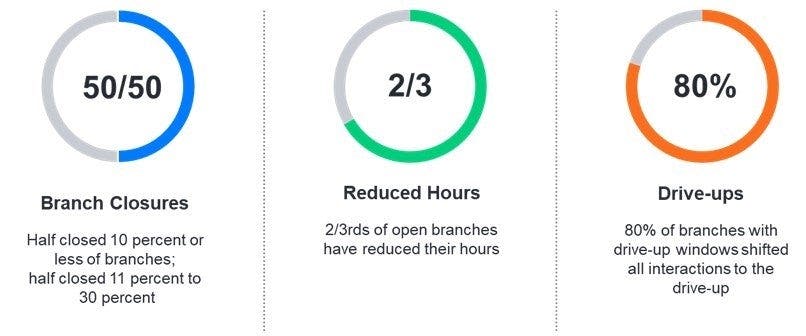

A recent survey of Kiran Analytics, Verint’s branch business unit, customers representing nearly 40,000 branches showed widely varied responses to the pandemic.

And when asked about how they are handling their branch staff, the answers varied. Some financial services firms have:

- Utilized excess branch resource capacity to support contact center associates

- Leveraged branch staff working from home to support the chat channel

- Staff member helping small business customers with their PPP applications.

Regardless of how they responded, all retail banking leaders confirmed that the “human” element played a huge role in their organizations’ ability to adapt and respond to customer and staff needs in light of the pandemic.

Future Predictions

There is no question that in-person banking in branches will be different going forward. We asked survey participants questions about the future of branch banking including:

- Branch Closures: About 80% of our survey respondents anticipated that fewer than 10% of branches currently closed would remain closed in 6 months.

- Operating Hours: About 60% of bankers expect modest reductions in open hours to remain post-COVID.

- Channel Support: They anticipate some work from the contact center to be shifted to the branch resources.

So, what do all these changes mean for financial services firms? Let’s explore the risks, challenges and possible actions executives can take to adapt branch banking to the new normal.

Risks

These sudden and dramatic changes present financial institutions with two risks to retaining and growing their customer base:

- Customers will feel pushed into digital-only banking relationships, which tend to have lower customer satisfaction and retention scores.

- Growth will suffer if bank branch realignment decisions underestimate the fact that the physical channel remains the most effective way to capture new customers and expand relationships.

Banking leaders need to balance these risks with the opportunity to redefine the branch experience for both the customers and the workforce in the new normal. They need to realign branch delivery with decisions driven by data and branch analytics, instead of intuition or one-size-fits-all approaches.

Let’s look at how modeling and branch analytics can help.

Branch Banking Challenges and How Realignment Modeling Can Help

Assessing the Direction and Magnitude of Shifts in Customers’ Channel Usage

In the last few months during the pandemic, survey bankers reported 30-40 percent drop in branch transactions. Given this dramatic drop, and anticipation of a slow recovery, you might be thinking of closing or consolidating some branches. If you do close a branch in a specific market:

- How much customer activity and work content will migrate to which nearby branches?

- How much work content will move to other channels or competitors?

- What will be the FTE requirements in the remaining branches?

Modeling the direction and magnitude of the shifts in work content can help analyze the impact of changes within each market in order to properly staff the branches and meet customer demand.

Optimally Allocating Fixed Resource Capacity for Maximum Efficiency and Effectiveness

Temporary branch closures, open hour reductions, and service restrictions are necessary to address customer and associate safety at this time. But, what happens when post-pandemic budgetary constraints require assessing what-if scenarios, such as:

- Which branches in which markets are the best candidates for closing permanently?

- What adjustments to the open hours will produce the greatest efficiency?

- What are the optimal queue configurations in each branch?

- How should the FTE be optimally distributed, by position, to the branches with the greatest potential and opportunity?

Modeling the distribution of available FTE, by position, can help analyze the impact of changes such as branch closures, open hours adjustments, and service touchpoints to address this strategic challenge.

Streamlining Branch Operations for Operational Efficiency

Slowing deposit growth, narrowing interest margins, and increasing competition from digital banks will continue to put enormous pressure on retail bank branches to improve operational efficiency.

Given nearly half of a retail bank’s operating expenses consist of facilities, workforce, and branch support, streamlining initiatives will accelerate as the pressure to increase operational efficiency intensifies.

Click here to learn about five specific initiatives for streamlining branch operations and how such initiatives, when driven by branch analytics, have paid off for branch transformation leaders.

Bank Branch Realignment Strategies Driven by Branch Analytics

Branch channel and workforce realignment strategy and tactics will be unique for each financial institution.

Overlaps created by mergers and acquisitions in the past few years may accelerate branch consolidation and staff reductions for some financial institutions. They may keep 10% or more of their branches closed permanently and use digital engagement to replace in-person service.

For many financial institutions, the evolution of the branch channel and workforce has been underway for a decade. They have been reducing the number of branches, deploying technology, and implementing a minimum staffing model with universal bankers in many branches. They may utilize open hours, queue configurations, and resource pooling as primary levers of their branch realignment strategy while making slight reductions to branch counts.

No matter what the realignment strategy, the complexity of the decisions will require data, proper modeling, and advanced branch analytics. Prudent banking leaders should ask themselves:

- Are we able to model the direction and magnitude of shifts in customers’ use of the branch channel, given the drastic changes to the network and staffing caused by COVID-19?

- How can we optimally allocate fixed FTE to our branches while modeling alternative scenarios such as branch closures and hours adjustments?

- Do we have the right branch analytics solutions to accelerate our streamlining initiatives?

If you need help answering these questions, or support for your branch channel and workforce realignment initiatives, we can help. Contact us to learn more.

Related Content:

Bank Branches: There’s No Going Back to Pre-COVID Days

Branch Workforce Engagement: The Key to Improving CX in Retail Banking